Investment Thesis

I am currently “neutral” on E.ON (OTCPK:EONGY) (OTCPK:ENAKF) as its share price accurately balances the growth prospects of realised synergies and green investment, with the risks of decreased demand and operational changes that the company is undertaking.

Company Summary

E.ON is an energy company headquartered in Essen, Germany. It is the network operator in countries such as Germany, Sweden and a series of countries in Central-East Europe. Concurrent to this, it offers retail services across Europe in countries like Germany, the UK, the Netherlands, and Belgium. It currently operates these two businesses in segments called Energy Networks and Customer Solutions. It used to have a segment called Renewables; however, the majority of these assets have been transferred to RWE (OTCPK:RWEOY) in a complex asset swap that involved E.ON gaining management of the company called Innogy. The full integration of these assets was complete as of January 1st 2020. Non-core assets include the energy generation business in Turkey and the decommissioning of Nuclear assets in Germany.

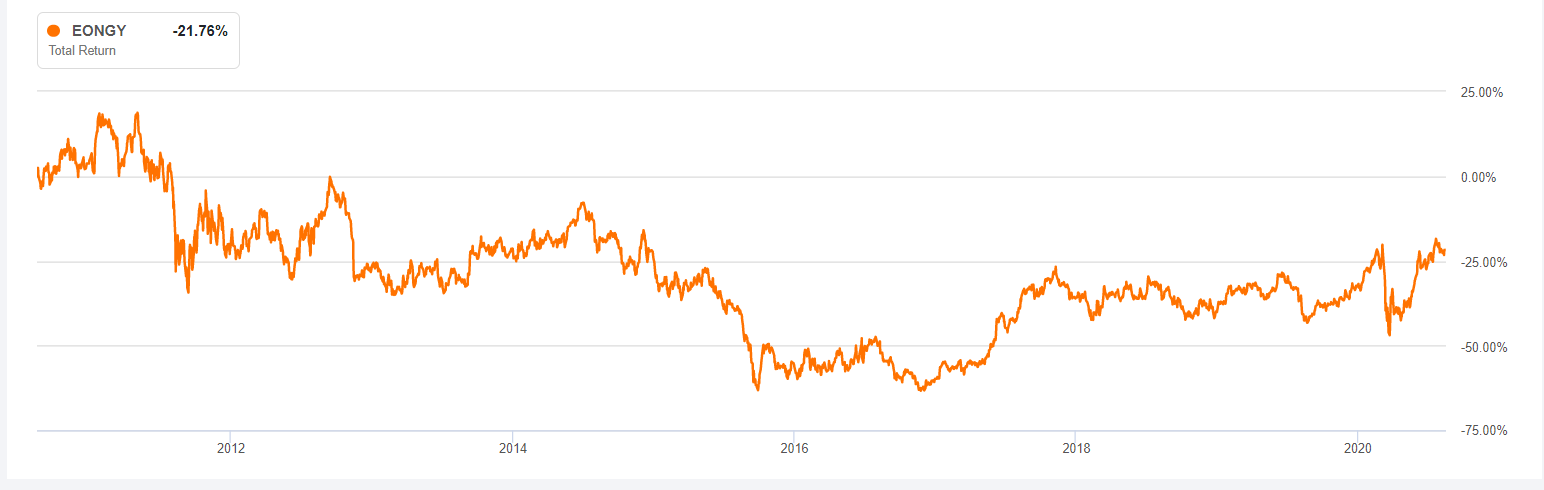

Figure 1 – E.ON 10-year total return.

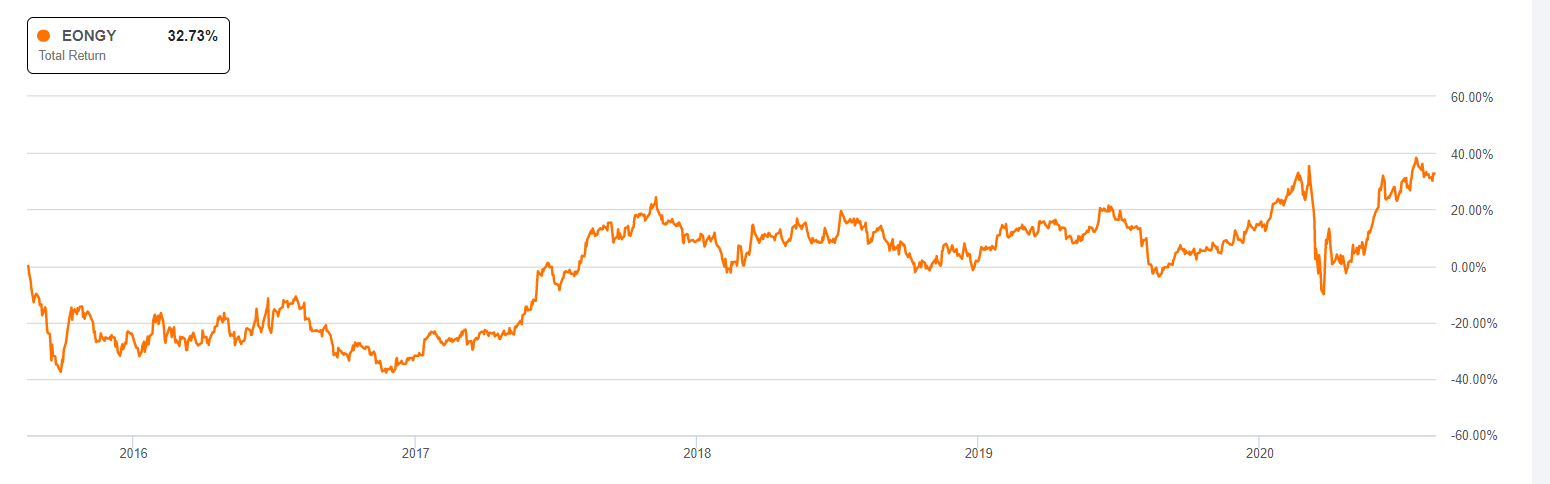

Figure 2 – E.ON 5-year total return

The total return over the past 10 years has been poor; however, after the trough in 2016/17, the company has been on an upwards trajectory. This impact mainly came from the decommissioning of nuclear assets as Germany sought an exit from nuclear by 2023. This led to massive provisions being taken at a time of very low energy prices due to oversupply. The incentives set by Germany and the EU lead to massive amounts of renewable infrastructure being created thus causing diminishing asset returns. In 2016, E.ON split off its fossil fuel assets into a company called UNIPER (OTC:UNPRF) while retaining a stake in the company. It was then bought out of this position by the state-owned Finnish company Fortum (OTCPK:FOJCF) (OTCPK:FOJCY). Since then, the company has become profitable, increased its payout ratio, and diversified across different businesses and regulatory boards.

So, what is the future outlook for the company after this complicated asset transition? How has the value of the company changed and does it deserve the 28% surge in stock price it has seen over the last year?

Strengths

On the broadest levels, E.ON has the advantage of diversification. It is present across most of the energy value chain and is diversified across regulatory bodies. This creates revenue resilience to political changes of a single country. Intangibles like brand, customer satisfaction and its innovation track record are all well above average.

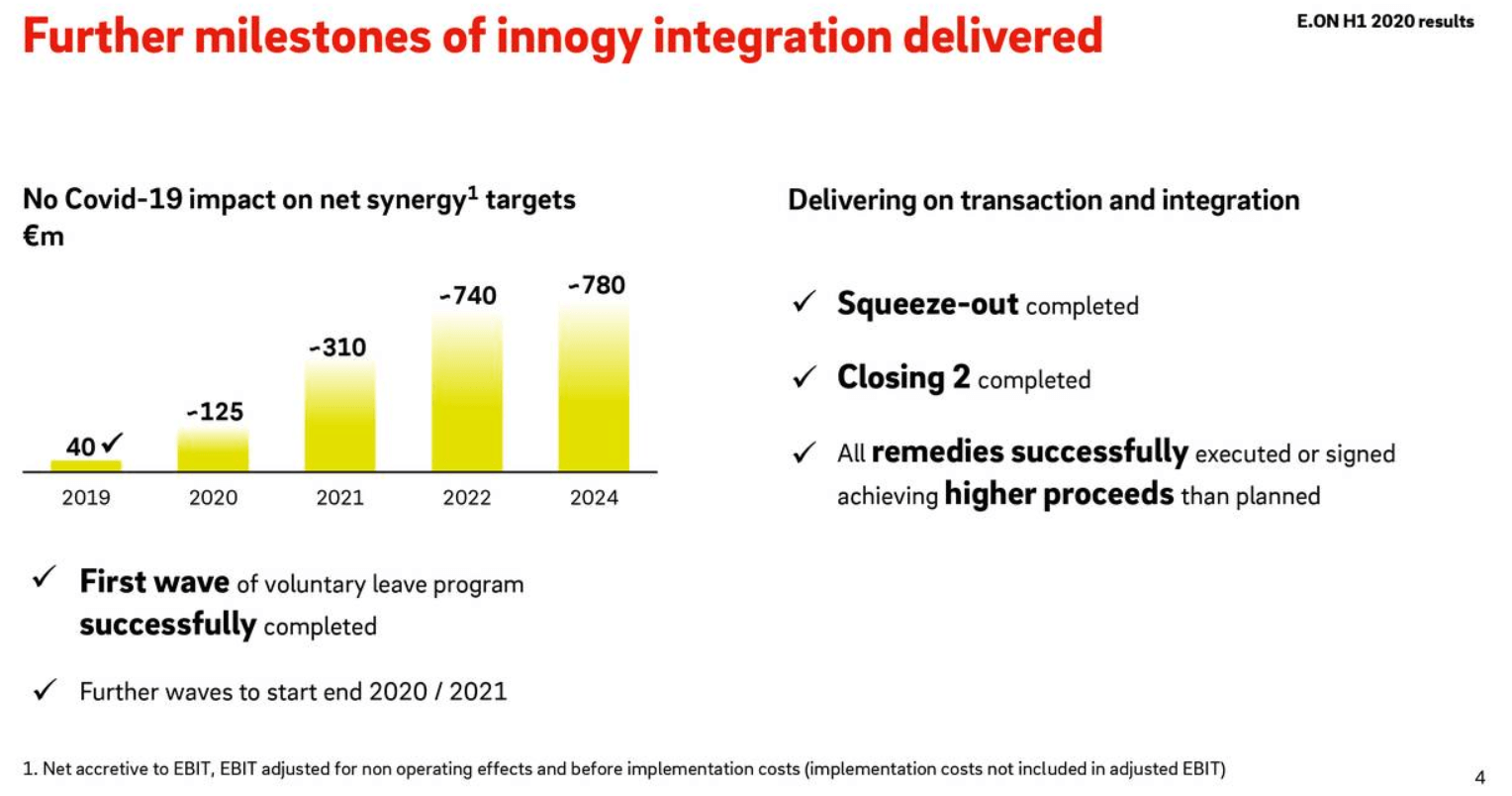

Through the purchase on Innogy and the sale of the Renewables section, E.ON has streamlined its network and retails sections. All of the Innogy assets have been integrated into these sections and the company expects to realise significant synergies.

Figure 3 – Expected Innogy synergies from Q2 2020 Earnings report

In the Q2 2020 earnings call, Johannes Teyssen (Chairman of Management Board and Chief Executive Officer) said:

One of the promises is the delivery of the €740 million synergies by 2022. Despite COVID, we are fully on track to deliver this plan for 2020 and beyond.

These synergies will help to grow the business and create value for the shareholder, yet will see diminishing returns after that. Innogy also contained one of the largest European EV (electric vehicle) charging networks with approximately 5,300 charging points in over 20 countries.

Another initiative that improves the company is its intensive investment into the digitization of its customer platforms. This allows for the increased processing of data which can improve services and efficiency, especially if AI customer service was implemented. It predominately operates these cloud-based platforms in Germany and the UK, although will likely expand them. By 2022, E.ON intends to have migrated all of its customers in these two countries to its cloud-based platform. It will has partnered with SAP (NYSE:SAP) in Germany and Kraken Technologies which is an affiliate of Octopus [LSE: OOA]. Octopus Energy is currently ranked as the “Which?” top provider with the joint best digital tools. Mimicking this process will increase service capabilities.

Weaknesses

E.ON still must decommission all its nuclear assets. Whilst provisioning has occurred, the risk is always present that more CapEx is required. It is an arduous process, and even though the German government ensured the entire sector contributed to the construction of storage facilities, costs may still (likely) overrun.

By bartering away its renewable energy generation assets to RWE in exchange for Innogy, E.ON has limited its access to the value chain. Whilst certain assets have remained with the company, it has minimised its access to funding to prepare the UK and the EU to be carbon neutral by 2050.

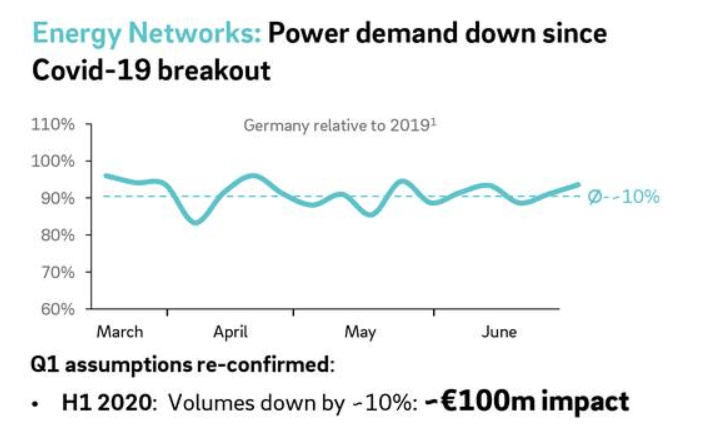

Mild seasonal weather and COVID-19 have impacted energy demand as businesses have been closed.

Figure 4 – Decreased demand due to mild weather and COVID-19 H2 Report

Although the company believes these revenues to be recoverable due to the current regulatory schemes, I still see this as uncertain. In its earnings reports, the company was more positive than I about the future involving COVID-19. The company has also admitted that it believes the UK business will be loss-making this year. The UK struggled to handle the pandemic, and this will definitely impact the consumption of peripheral energy services.

Opportunities

I am incredibly bullish on the growth in the EU and UK green energy sector. I have recently completed articles on Drax Group (OTC:DRXGF), Centrica (OTCPK:CPYYF), EDF (OTCPK:ECIFF) and SSE (OTCPK:SSEZF) (links at the end) that are set to capitalise on this. E.ON’s exposure to the investment promised by the EU in the Green New Deal and the Recovery Plan is well summarised in the slide below.

Figure 5 – EU investments that E.ON would be eligible for – H2 Report

E.ON is able to compete for incredible sums of money that are being invested in the economy. European governing bodies have all decided that the investment they provide to counteract COVID-19 should kill two birds with one stone. Investment in renewable technology and infrastructure is a vote-winner, therefore they can stimulate the economy whilst driving forward green energy growth. E.ON is set to benefit from this.

E.ON currently participates in a lot of renewable energy projects. It has over 50 hydrogen gas-related projects in production, distribution and storage, along with retail projects that will help to increase the efficiency of developments.

EVs have had global CAGR of over 19% estimated by analysts. The acquisition of Innogy has positioned it as market leader behind companies like EDF. It has the resources to implement charging stations throughout Europe and benefit from the transition of care energy demand from fossil fuels to the electric gird.

It is expanding internationally predominately into Eastern Europe. However, it could follow in the footsteps of companies like EDF and expand continentally into the Middle East where there are extensive investment prospects.

There is also considerable growth to be recognised in its heating district assets. These assets operate by providing the households in an area with heat from a centralised location. This could be in the form of hot water or space heating. There is strong research to suggest that this is more efficient than localised heating systems (boiler in each house). Fortum has recently sold a series of these assets for x25 EBITDA values. This implies that there is strong growth potential in this method.

Threats

Whilst a sizeable amount of infrastructure and customer services must be implemented to realise the carbon-neutral economy by 2050, E.ON is not in the best position to realise this. The sale of its renewable energy assets deprives the company of the potential investment into this area. It has allowed its competitor, RWE, to dominate this space. A lot of the company’s networks can be retrofitted to suit the new energy generation methods. This disadvantages it from companies that overlap their business and also generate energy.

E.ON instead seems to be positioning itself to benefit from the move away from natural gas. It has done this by investing in hydrogen projects. However, natural gas is not prioritised for funding to achieve carbon neutrality. In the very long term, its leadership may represent a significant moat; however, before then I see this being a costly and may suffer from the unrecognised value in comparison to projects removing more pollutive assets from the ecosystem.

A resurgence in Europe of the COVID-19 pandemic will lead to lower energy consumption. This would delay the planned recouping of losses that it has suffered so far during 2020. Also, if the company has incorrectly estimated the amount of bad debt, then losses may also be more significant.

Smaller retail service companies are growing in strength. Operating in the retail sector requires little start-up capital and so the moat surrounding this section is small.

The European markets are heading for further consolidation to create efficiencies and even manufacture a European super grid across mainland European countries. Therefore competition laws on network companies will have to be relaxed. This does not benefit E.ON because it becomes exposed to state-owned companies in Europe with political power influencing decision making. This could lead to it being edged out or not price competitive as there is a supply influx from countries like France that have much less taxation on nuclear assets.

Financials

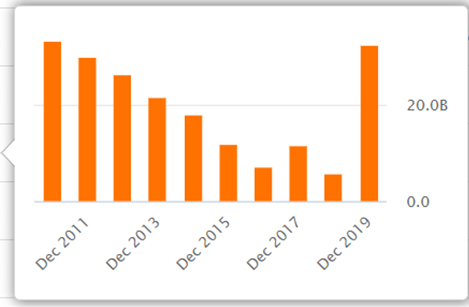

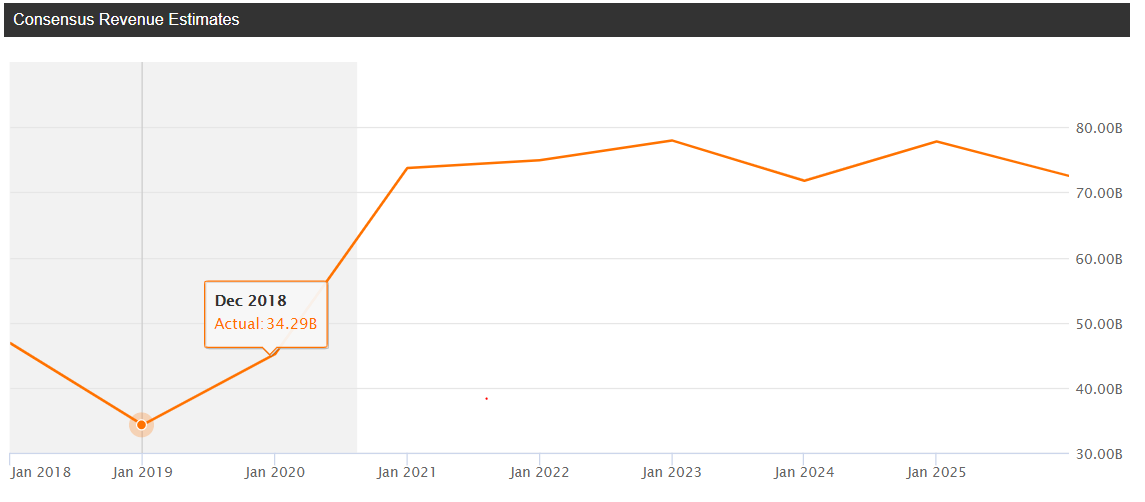

Due to the Innogy asset swap, the financials are a little hazy. Net debt has jumped massively, but expected revenues have also increased.

Figure 6 – Net Debt SA Financials

Figure 6 – Revenue Estimates from SA Earnings

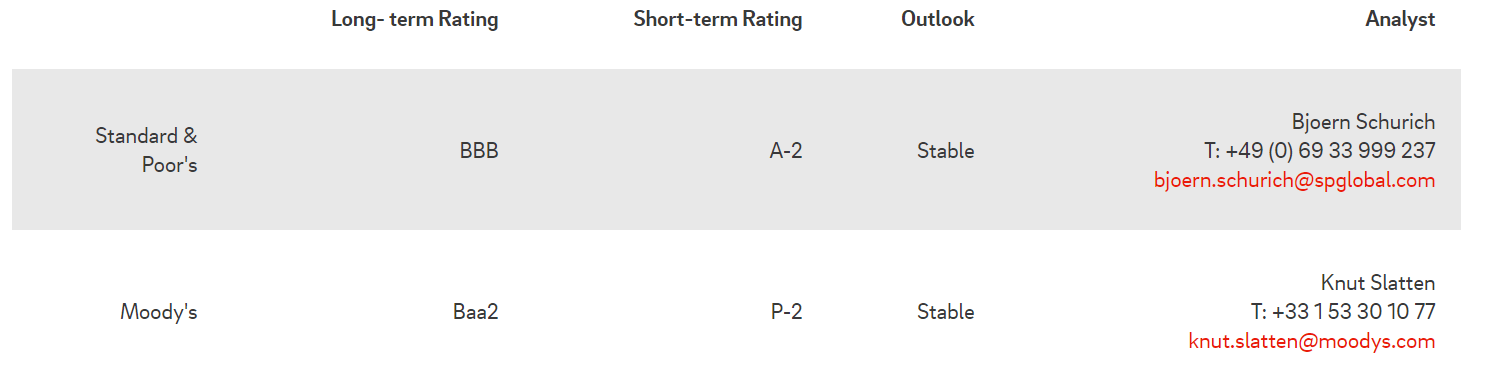

The net debt/EBITDA in 2018 was about 1.62x, whereas currently, it is 6.24x. This has increased the ratio by nearly 3.9x. Projected EBITDA is expected to increase this year to €6.8-7 billion. However, the net debt level is also forecast to increase to €43 billion. This leaves us with a ratio at approximately 6.14x. This is a sizeable debt load. In this low rate world, the debt coverage is not affecting the company unduly; however, long term, it is unwise. Current credit rating is strong despite the turmoil due to the perceived stability of the regulated utility markets. E.ON intends to have lowered this ratio to approximately 5x by 2022. To pursue both growth and efficiency can counteract one another. However, if the company can achieve it, then it will emerge very strongly.

Figure 7 – E.ON’s credit ratings

The company’s estimation of growth is very impressive. This amount of growth in a large-cap utility has caused a lot of attention, hence the trailing P/E ratio is at 35.16x.

Figure 8 – Growth Estimations in H1 2020

The company also expects RAB (Regulated Assets Base) to grow at 4-5% per year and has recently revised this from 3-5%. However, current earnings per share (EPS) forecasts for 2020 are €0.65, although this seems conservative as H1 EPS was €0.36. So, assuming an EPS of €0.7 at a CAGR of 22% for the next two years, we get a 2022 EPS of €1.01. At the current price of €10, this is only a P/E of 10x, which is good but not incredible value.

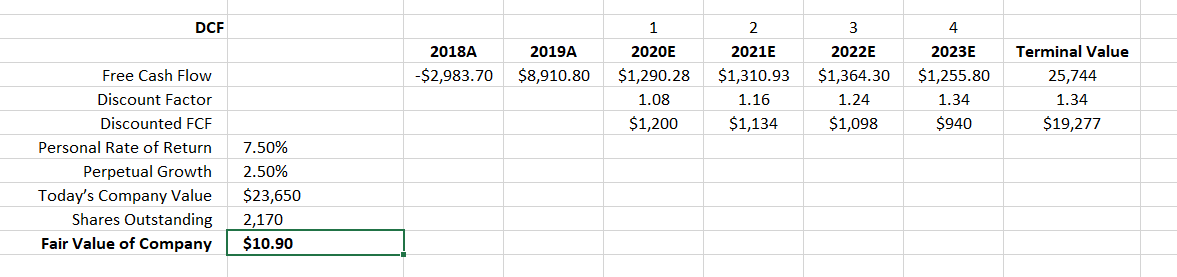

Valuation

In this section, I will use a DCF model (in $) to estimate a company fair value. I will then apply my preferred discount (10%), my level of calculation confidence discount (5%) and the COVID-19 discount (5%).

Figure 9 – DCF model by author

Figure 9 – DCF model by author

This DCF model calculated fair value of $10.90 for the company using from SA revenue estimates. This is conservative as it was hard to calculate the appropriate net income margin and net income to FCF ratio. To do this, I used 2.5% as the net income margin as this fell within the ANI (Annual Net Income) range forecast by E.ON from the consensus revenue estimates.

Therefore, my personal entry price would be at $8.72 during these uncertain times. I believe that the stock is fair valued; however, its headline CAGR will likely encourage investors and bump the price up further.

Conclusion

I am currently “neutral” on E.ON as its share price accurately balances the growth prospects of realised synergies and green investment, with the risks of decreased demand and operational changes that the company is undertaking.

It has excellent bottom-line growth prospects through synergies and top-line growth through international expansion and investment to create a greener energy sector. However, it is going through radical operational changes creating higher levels of risk and carries a significant level of debt which may hinder it going forward.

It could suffer going forward as it does not have a presence in renewable generation anymore, and therefore is at risk of missing out while others gain. Companies like EDF (article here) and SSE (article here) are across the entire value chain and will profit because of it. They are also in much more stable positions with little flux likely in the future, also EDF trades at 0.6x price/book, unlike EON which is at 4x. Whilst CapEx is high, they have a wide moat and it is difficult to affect their earnings potential.

Conversely, it lacks focus. Centrica (article here) is in the process of becoming an entirely retail orientated business which will turn it into a cash flow machine if it can do it correctly. On the other side of the spectrum, Drax (article here) has been generating electricity for years and has recently jumped to renewable energy generation.

Therefore, E.ON may either be in the Goldilocks zone and have the best of both free cash flow and a wide moat or it may lack focus and miss out on valuable asset base investment. Only time will tell.

If anybody has any thoughts on the article (be they positive or negative) I would love to hear them! I really want to improve and I want the reader to shape the content I create. Stay safe – Tom

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in DRXGF, CPYYF, SSEZF over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.